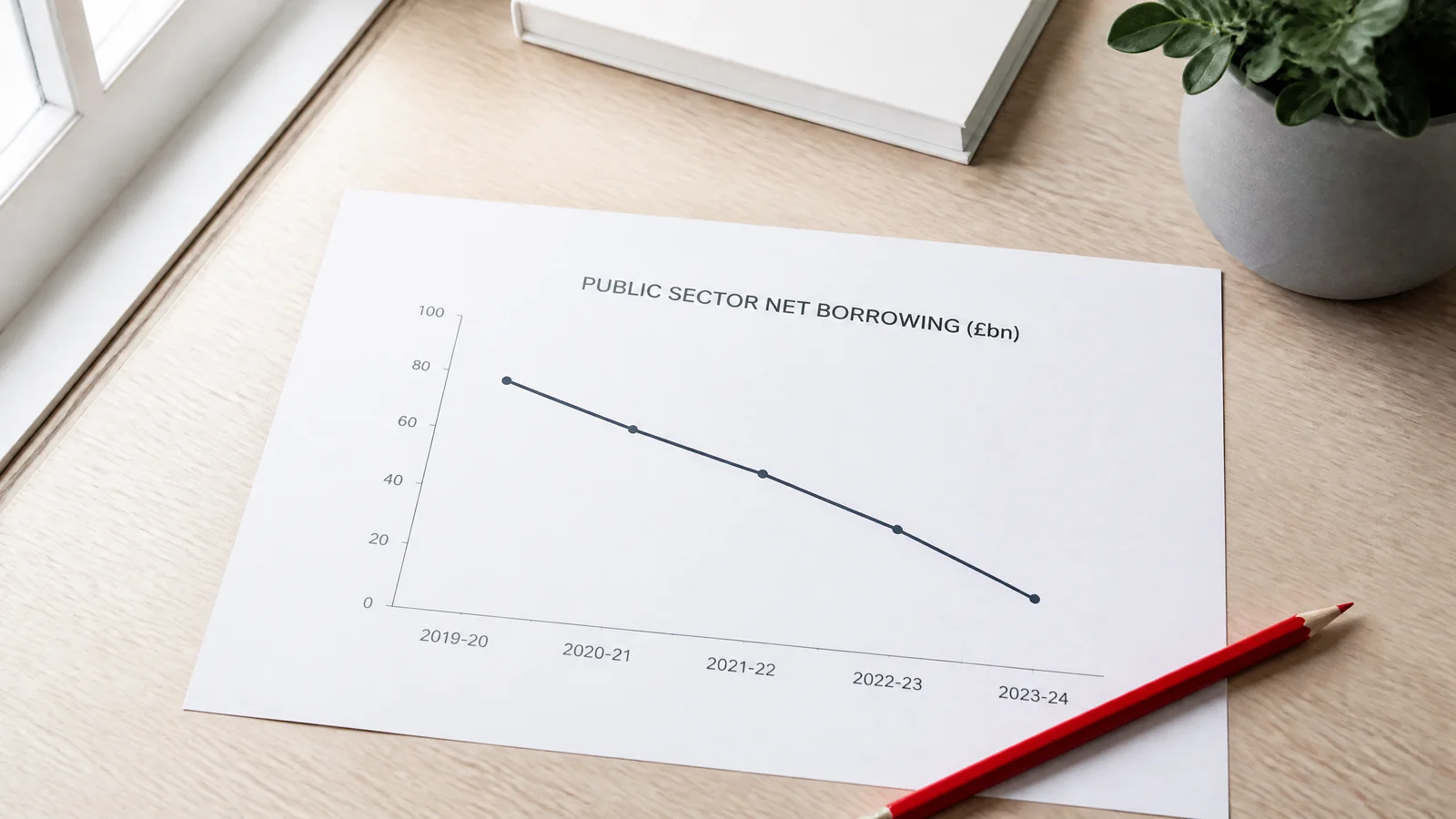

The recent news of lower-than-expected government borrowing in December, as reported by the Office for National Statistics (ONS), presents a fascinating case study in fiscal management and its implications for economic policy. This development, marked by a borrowing figure of £7.8 billion, significantly less than anticipated and the lowest for December since 2019, prompts a critical analysis of the possible consequences and the options now available to the government.

Firstly, it's imperative to understand the context: government borrowing essentially measures the deficit between spending and tax income. A reduction in this borrowing suggests either increased revenue, decreased expenditure, or a combination of both. In this instance, a sharp decline in interest payments, linked to a notable fall in inflation, has played a pivotal role. The government's interest payments are tethered to the Retail Prices Index measure of inflation, and as inflation decreases, so does the cost of servicing debt.

Now, the question arises: what does this mean for future economic policy, particularly in the context of the upcoming Budget? Ruth Gregory, Deputy Chief UK Economist at Capital Economics, and others have suggested that these better-than-expected figures could provide the Chancellor with "wiggle room" for tax cuts in the spring Budget. Tax reductions are often viewed as a stimulant for economic growth, ostensibly by increasing disposable income for consumers and reducing the burden on businesses. This perspective aligns with Chancellor Jeremy Hunt's comments at the World Economic Forum, where he hinted at a desire for tax cuts, associating lower taxes with more dynamic and faster-growing economies.

However, the decision to implement tax cuts must be weighed against several factors. For one, the government's fiscal rules mandate a balance between spending and borrowing. While the lower borrowing provides some leeway, there's a need for cautious optimism. A temporary dip in borrowing should not be conflated with long-term fiscal stability. Moreover, the UK's total debt stands at a staggering £2.67 trillion, approximately 97.7% of the GDP. This level of indebtedness, comparable to the early 1960s, necessitates prudent financial management.

Furthermore, the broader economic context cannot be ignored. The government's fiscal policy during the Covid pandemic and the subsequent energy crisis following Russia's invasion of Ukraine led to a significant increase in borrowing. While these were necessary measures to protect lives and livelihoods, as noted by Chief Secretary to the Treasury Laura Trott, they have resulted in substantial debts that need to be managed judiciously.

In conclusion, while the opportunity for tax cuts presents itself, it must be approached with a careful balancing act. The government needs to ensure that any such measures do not jeopardize fiscal sustainability or overlook the necessity of debt reduction. It's imperative for policymakers to deliberate these decisions thoroughly, considering both short-term gains and long-term economic health.

The Partner Still Signs

A weekly briefing on AI, accountancy and professional judgement, from inside a Manchester practice established in 1948. Evidence, not confidence.